Exemptions

ASSESSORIn addition to assessing value to property, the Assessor also manages exemptions from property taxes. Here you will find more information on the various exemptions. Each type of exemption has it’s own unique application process – none are automatic. If after reading this information, you have more questions or would like to request an application, feel free to contact us as 2cAsr@canyoncounty.id.gov

Homeowner’s Exemption Application

The homeowners exemption is a program that reduces property taxes for individuals who own and occupy their home as their primary residence. This is done by reducing the net taxable value of the home and up to one acre of land by half (up to a certain maximum). Beginning in 2021 the maximum homeowner’s exemption reduction moved to $125,000 and will remain that amount until the legislature changes it. Previously the maximum reduction was adjusted annually using the House Pricing Index for Idaho (HPI) published by the Federal Housing Finance Agency (predecessor to the United State Office of Federal Housing Enterprise Oversight).

| Year | H/O Max |

|---|---|

| 2021 | $125,000 |

| 2017 | $100,000 |

| 2016 | $94,745 |

| 2015 | $89,580 |

| 2014 | $83,920 |

| 2013 | $81,000 |

| 2012 | $83,974 |

| 2011 | $92,040 |

| 2010 | $101,153 |

| 2009 | $104,471 |

| 2008 | $100,938 |

| 2007 | $89,325 |

| 2006 | $75,000 |

| 1983-2005 | $50,000 |

| 1980-1982 | $10,000 |

How it Works

For a property consisting of a home and one acre or less of land with a total assessed value of $250,000 in 2021, the homeowner’s exemption would reduce the net taxable value to $125,000 – half of the total assessed value. In this example, the property owner would pay taxes on $125,000 even though the total assessed value is $250,000. This could cut the property tax bill in half!

If the same property’s total assessed value is $300,000 in 2021, the homeowner’s exemption would only reduce the net taxable value to $175,000. This is because half of the total assessed value is more than the maximum reduction for 2021. Instead of dividing the total assessed value by half, the maximum reduction is subtracted.

The value of other structures besides the home and the value of land beyond one acre is not reduced by the homeowner’s exemption.

How and When to Apply

To qualify for a homeowners exemption, it is necessary to own and occupy the home as your primary residence. See Idaho Code 63-602G The application may be filed any time after you purchase, move in and make the home your primary residence. Applications that are repopulated with the parcel and ownership information may be requested after the deed has been recorded and worked in our system. Depending on the volume of deeds coming through it could take a month after a deed has been recorded for the ownership to be updated in our system. To see if the ownership has been updated, you may view property ownership online using our Parcel Information database.

When we approve a homeowner’s exemption application we mail a receipt to the applicant. This receipt should be kept in a safe place for as long as you own the home. Applicants should not assume they have a homeowner’s exemption until they have received this receipt.

When the Homeowners Exemption takes Effect

The homeowner’s exemption will take affect on the date of a completed application. If the previous owners had a homeowner’s exemption, and did not apply for a homeowner’s exemption on a different property for that year, the exemption will remain active until the end of that calendar year. However, it is not advisable to depend on gaining the benefit from the previous owner’s exemption. Always apply for your own exemption as soon as you are eligible.

If you would like to know if a home currently has a homeowners exemption or would like to request an application you may contact us at 2cAsr@canyoncounty.id.gov.

Maintaining Exempt Status

Once you qualify for this exemption, you do not have to re-apply unless you move or record a new deed. Even if you only change your name or even the spelling of your name and record a new deed to reflect these changes, you may need to re-apply for a homeowners exemption. This is because the Assessor has no way of knowing that these two different names belong to the same person. Sometimes a new deed is recorded during a refinance and inadvertent changes to your name may happen. Always check on the status of your homeowner’s exemption after refinancing.

The assessment notice will indicate if there is a homeowner’s exemption on a property. For most types of properties, assessment notices are mailed in May. The net taxable value on that notice will be used to calculate the taxes on the bill that is mailed the following December. If the total assessed value matches the net taxable value, there is not an active homeowners exemption for that year. If the homeowner’s exemption (or anything else) is incorrect on the assessment notice, contact the Assessor BEFORE the deadline printed at the top.

When in doubt, always contact the Assessor at the email address above to verify your exemption status or how an event may impact your exemption status.

New Construction

If your home is newly constructed and no one has ever lived in the home prior to you, you must apply for the homeowner’s exemption within 30 days of being notified by the Assessor that the home has been appraised. Applications received later will be considered the following tax year. For more information on new construction taxes see What is an Occupancy tax?

Trusts and LLC’s

If you place your home in a Trust or LLC, it is necessary to provide the Assessor’s office with documentation stating who benefits from Trust of LLC per Idaho Code 63-703(4). The easiest way to do this is bring all of your Trust or LLC documents to the Assessor’s office. Staff will only make copies of the pages necessary to comply with Idaho code.

The agricultural program, also known as the ag exemption, reduces the taxable value of agricultural land.

Idaho Code describes agricultural land as: land actively devoted to agriculture and a part of a bona fide profit-making agricultural venture. The land is further described as follows.

- Used to produce field crops (and / or)

- Used by the owner or bona fide lessee for grazing of livestock to be sold as part of a net profit-making enterprise

- Land shall not be classified or valued as agricultural land which is part of a platted subdivision with stated restrictions prohibiting its use for agricultural purposes

- Land utilized for grazing of a horse or other animals kept primarily for personal use or pleasure shall not be considered to be land actively devoted to agriculture

Acreage Requirements

If the total area of such land, including the home site, is more than five contiguous acres (may be a group of separately assessed parcels with common boundaries), the owner may make initial application for the program. To continue the agricultural classification in future years, the owner must then ensure that the land continues to be devoted to agricultural use or show that it has been placed or continues to be in a crop retirement or rotation program.

When the area is five acres or less, such land shall be presumed to be non-agricultural land until it is established that the requirements below have been met.

- The owner must make an initial application and must show that the land was actively devoted to agriculture during the last three growing seasons (and)

- Agriculturally produces for sale or home consumption the equivalent of 15% or more of the owners’ or lessees’ annual gross income (or)

- Agriculturally produced gross revenues in the immediately preceding year of $1,000 or more, including net income per sale of livestock

- The landowner must provide proof of these minimum incomes each year for the land to remain in qualification

Application Deadline

Initial application must be made in the Assessor’s office by March 15th of the year in which the owner is seeking the agricultural classification on the land. For land that is five acres or less in size, the landowner must provide proof of income (from the year before) by March 15th each year.

Valuation of Agricultural Land

When property is accepted into the agricultural program, it is given one of the following classifications: dry cropland, irrigated cropland, dry grazing, or irrigated grazing. There are a number of different assessment rates that apply to the land according to its ability to produce crops or grazing grasses. The value is calculated by multiplying the acres in the program by one of these rates, which are lower than the per acre rates for full market value. These rates are provided by the State Tax Commission, and change each year.

For more information contact the Farm Department in the Assessor’s office at 2cAsr@canyoncounty.id.gov or 208-454-6655.

Habitat Improvement Program

Property that is part of an approved Habitat Improvement Program (HIP) is also eligible for the agriculture exemption. HIP projects are approved and managed by the Idaho Department of Fish and Game. Once the project is in place, provide a copy of the completed HIP contract to the Assessor’s office to begin receiving the agriculture exemption.

Property tax exemptions are available for certain types of nonprofit organizations. Religious, fraternal, educational and certain hospitals are a few examples of types nonprofit organizations potentially eligible for a property tax exemption in Idaho. It is important to understand the difference between property tax exemptions and other types of exemptions granted by other government offices such as the IRS or the State of Idaho. It is a common misconception that once an organization is granted an exemption from the IRS under 501(c)3 that all other exemptions will just be granted accordingly. This is not true in the case of property taxes.

Property tax exemptions are NOT granted automatically and must be applied for annually.

Part of the reason an application is required for a property tax exemption is that just being a nonprofit and owning property is not enough to qualify. In addition to owning the property, the organization must use the property exclusively for the purpose their organization is organized. Exemptions will not be granted on future building sites, on leased space or on space that is not being used. Only property that is currently being actively and exclusively used for a purpose related to the organization’s objective will be considered for a property tax exemption.

Applications for property tax exemptions can be requested through our email: 2cAsr@canyoncounty.id.gov. To see if there is an exemption available for your organization, examine chapter 6 of title 63 in Idaho Code.

It is important to complete all portions of the application fully, legibly and accurately and to include all requested supporting documentation. This application along with all pertinent documents must be returned by April 15th of the year you wish to receive the exemption. If more information is required to make a decision, you may be asked to appear in a hearing before the Board of County Commissioners.

Exemptions are granted for only one year at a time. After an exemption is first granted, a courtesy declaration may be mailed for the annual renewal. Failure to complete and return this declaration by April 15th will result in the removal of the exemption.

A homestead exemption is different than a homeowners exemption and not handled in the Assessor’s office. The terms homeowners exemption and homestead exemption are often used interchangeably, which is not accurate. Since there is so much confusion between the two programs, a short description will be given here. For more information regarding your specific situation, contact a real estate attorney.

A homestead exemption protects the owner’s equity in their property. Every property owner in the state of Idaho that occupies their home as their primary residence is automatically protected up to the first $100,000 in equity regardless of size per Idaho Code 55-1003. There is no need to file any paperwork in this case. The protection is applied automatically.

If you wish to have this exemption applied to unimproved land or property that you are not occupying, it is necessary to record a ‘Declaration of Homestead’ with the recorder of the county that the property resides.

A Declaration of Homestead must include:

- A statement that you intend to occupy this property as your primary residence in the future

- A complete legal description of the property

- The full cash value of the property

- A statement that this property can no longer be assumed a Homestead

- A complete legal description of the property

- Date of abandonment

If your property remains unoccupied, continuously, for six months the Homestead Exemption will be assumed to be abandoned per Idaho Code 55-1006. If an owner is going to be absent from the homestead for more than six months but does not intend to abandon the homestead, and has no other principal residence, the owner may record a declaration of ‘Non-abandonment of Homestead’ with the recorder of the county in which the property resides.

The declaration of non-abandonment of homestead must include:

- A statement that the owner claims the property as a homestead

- A statement that the owner intends to occupy the property in the future

- A statement that the owner claims no other property as a homestead

- A statement of where the owner will be residing while absent from the homestead property

- The estimated duration of the owner’s absence, and the reason for the absence

- A legal description of the homestead property

Summary

If you live in your home, you do not need to file any paperwork. If you have any questions regarding a homestead exemption, please contact a real estate attorney. Assessor’s office staff is not qualified to give such advice.

What It Is

The site improvement exemption, also known as the Developer’s Discount, was signed into law in 2012. This law grants a property tax benefit to land developers under 63-602W. A need for this benefit was deemed after the recent crash of the housing market left numerous vacant subdivisions all over the state. The intent of this exemption is to provide some tax relief to land developers that have incurred the expense of building roads and bringing in utilities and other infrastructure and have been left with an inventory of buildable lots that they are unable to sell.

How to Qualify

A land developer who owns land that they developed, or caused to be developed, may qualify for this exemption but only on the parcels that have not been built upon. One who holds undeveloped land does not qualify for this exemption. Investors, banks or any other entity having purchased or repossessed developed land with infrastructure already in place do not qualify for this exemption even if they loaned the money used to develop that land.

How it Works

Application must be made to the Assessor on each phase of each subdivision for which the exemption is requested by April 15th. Applications can be obtained by contacting the Assessor at 2cAsr@canyoncounty.id.gov. In addition to the application, a spreadsheet must be completed. This spreadsheet itemizes the parcels in the subdivision for which the exemption is being requested. Staff will research the chain of title to ensure structures have not been built or begun to be built. Once all documentation has been provided by the applicant and researched by the Assessor a meeting is scheduled with the Commissioners to consider granting the exemption. Exemption decisions must be made by May 15th and the property owner is notified on their assessment notice that is sent by the first Monday of June. Parcels that receive the exemption enjoy a reduced net taxable value. The amount of reduction is the difference between the market value of the land with site improvements and the market value of the land without site improvements. In the event that the market value of land without site improvements cannot be reasonably assessed due to lack of comparable sales, a reduction of 75% off the full market value is given. The applicant is required to notify the county when a parcel is no longer eligible for this exemption by April 15th each year. The Assessor can provide a spreadsheet of currently exempt parcels to assist with this requirement.

How and When the Exemption is Removed

There are two events that would make a parcel ineligible for this exemption.

- Convey the property to another individual or company that the current owner does not have at least 50% ownership in

- Begin construction

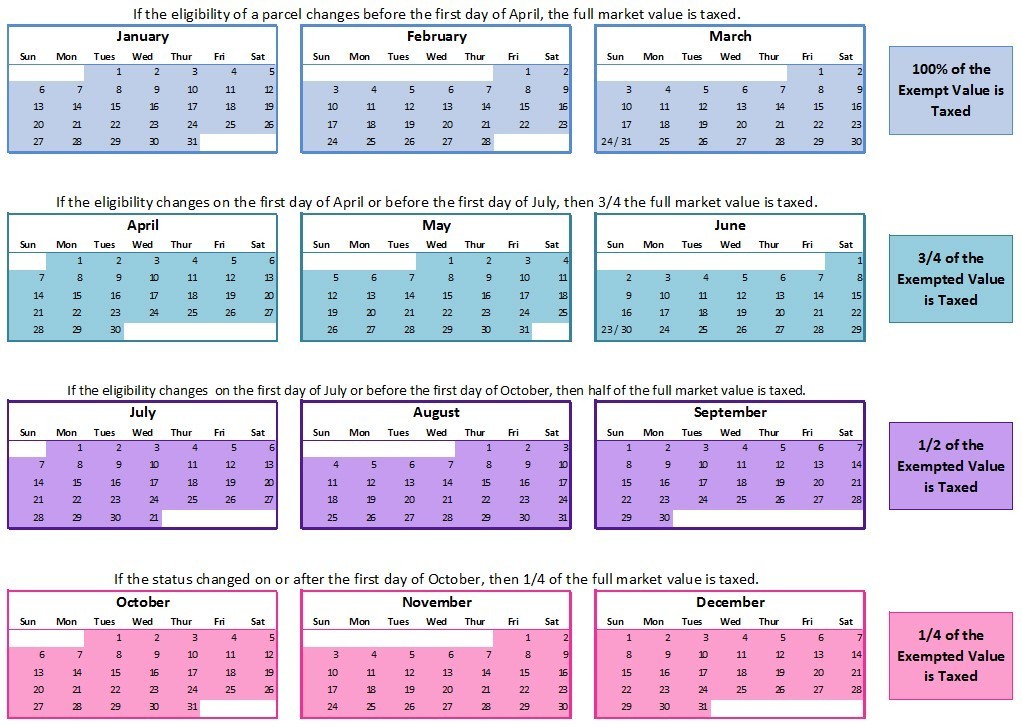

When the exemption is removed the taxes are pro-rated quarterly per Idaho Code 63-602Y. If the eligibility of a parcel changes before the first day of April, the full market value is taxed. If the eligibility changes on the first day of April or before the first day of July, then 3/4 the full market value (minus the exempted value already taxed on the regular roll) will be taxed on the subsequent roll. If the eligibility changes on the first day of July or before the first day of October, then half of the full market value (minus the exempted value already taxed on the regular roll) is taxed on the subsequent roll. If the status changed on or after the first day of October, then 1/4 of the full market value (minus the exempted value already taxed on the regular roll) is taxed on the subsequent roll. An illustration of these dates can be found at Exemption Removal Calendar.

How this Exemption Affects Buyers

When buying a newly built home in a subdivision that has the site improvement exemption a buyer could end up with three different tax bills in the months to follow.

- A bill from the regular roll for the exempted land. This bill is typically estimated at closing and the seller credits the buyer the estimated amount of taxes for the portion of the year they owned the land. Then the buyer is responsible for the full bill when it actually comes due. Since this bill is calculated on an exempted value it will be much lower than a bill on similar land without the site improvement exemption. This bill is sent by the Treasurer at the end of the year and is due December 20th.

- A bill from the occupancy roll for the newly constructed home. This bill is just for the new buildings (not the land) and is prorated for the number of months the home was occupied. This bill is sent by the Treasurer shortly after the first of the year.

- A bill from the subsequent roll. This bill is for difference between the exempted land value and the full value of the land. This is an additional bill generated because the prior owner had the site improvement exemption. Land that does not have the site improvement exemption would not incur this bill because the full value of the land would be taxed all at once on the regular roll. This bill is sent by the Treasurer shortly after the first of the year.

It would be prudent for a potential buyer to check the status of the site improvement exemption before choosing a subdivision to purchase from if paying an extra tax bill would be a hardship.

Unless other procedures are described for a particular exemption, Idaho Code 63-602Y governs how a property tax exemption is removed. The site improvement, agricultural, and nonprofit organization are just a few exemptions that are removed by this code. When the exemption is removed the taxes are pro-rated quarterly. If the eligibility of a parcel changes before the first day of April, the full market value is taxed. If the eligibility changes on the first day of April or before the first day of July, then 3/4 the full market value (minus the exempted value already taxed on the regular roll) will be taxed on the subsequent roll. If the eligibility changes on the first day of July or before the first day of October, then half of the full market value (minus the exempted value already taxed on the regular roll) is taxed on the subsequent roll. If the status changed on or after the first day of October, then 1/4 of the full market value (minus the exempted value already taxed on the regular roll) is taxed on the subsequent roll. Due dates for each of the different tax rolls can be found at Important Dates. The calendars below illustrate how much of the exempted value is taxed based on when the property becomes ineligible.

Main Assessor Location

111 N. 11th Ave Caldwell

Main Assessor - Suite 250

Plat Room - Suite 230

Rural Dept - Suite 220

Vehicle Registration Location

6107 Graye Lane, Caldwell

Vehicle Registration Online

MV@canyoncounty.id.gov

Auto License Contact

P 208-455-6020

F 208-454-6019

Main Phone / Fax

P 208-454-7431

F 208-454-7349

Office Hours

Weekdays 8am - 5pm

(excluding holidays)

DMV 8am - 4pm

(excluding holidays)